June 2026: Market Report

While headline inflation has remained stable this month, higher producer costs, rising labour expenses and ongoing supply chain disruption continue to place pressure on service providers.

Key Food & Beverage Movements

Although cooler spring temperatures have slowed the development of some UK-grown crops, the transition to seasonal British produce is now well underway.

Spring cabbage and kale, Jersey Royal and Cornish new potatoes, courgettes, leafy salads, strawberries and cherries are all showing good availability. UK blackberry production has also begun, providing a smooth transition from previous supplies sourced from Portugal and Guatemala.

Cooler conditions have created short-term pressure on raspberries and blueberries, while the switch to UK coriander and parsley has also been delayed following a wet winter and slow start to warmer weather. Some of these constraints are expected to ease as temperatures increase over the coming weeks.

Air freight disruption linked to the Middle East conflict continues to affect imported produce. Reduced capacity from Kenya has limited basil and chive supplies, while key freight hubs in Qatar and the UAE remain under pressure. However, suppliers report that overall availability is no worse than when the issues first emerged, despite higher freight costs.

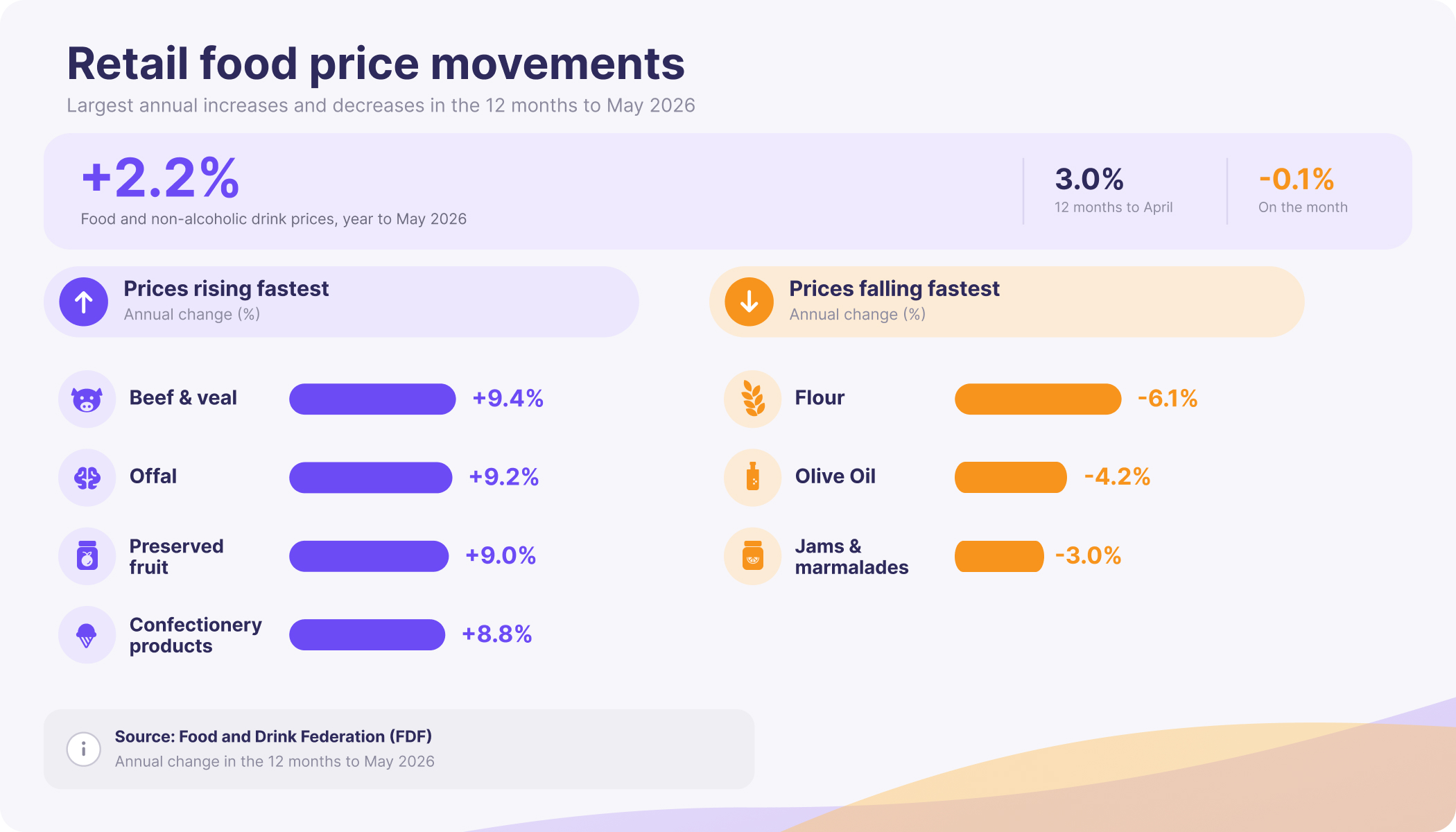

Overarching Market Pressures

Producer input prices rose 8.7% year-on-year — the largest annual increase since February 2023 — while producer output prices increased by 4.0%, driven primarily by higher crude oil and refined petroleum product costs. By comparison, consumer price inflation remained at 2.8%, with food and non-alcoholic drink inflation easing to 2.2%, down from 3.0% in April.

Karen Betts, Chief Executive of the Food and Drink Federation (FDF), said that this is because “it generally takes several months for the increased costs paid by farmers, processors and manufacturers to filter into raised prices at the tills” due to the widespread use of long-term contracts. The FDF therefore expects food inflation to strengthen again later this year as these higher costs feed through the supply chain.

As a result, consumers have remained cautious with their spending. This, combined with mixed weather at the start of the month, contributed to a slow start to June for drinks sales. However, warmer conditions and the start of the 2026 World Cup quickly helped improve trading, with UK pubs serving an estimated 5.5 million additional pints during the tournament so far.

Despite reports of positive sales momentum, service providers continue to face rising labour costs. Many operators say increases to the National Living Wage and employer National Insurance Contributions are restricting recruitment, particularly for entry-level roles. Some have warned that, coupled with sustained rises in energy prices, these pressures could ultimately result in further business closures.

Outlook and Opportunities

While some costs are unavoidable, others are often overlooked. Regularly reviewing supplier contracts can help identify surcharges, minimum order requirements and automatic price adjustments that may no longer be justified. Any additional fees introduced during periods of market disruption should be revisited and challenged where appropriate.

Alternative brands and equivalent products can also help protect margins. In many cases, operators can reduce purchasing costs by switching to products that offer comparable quality without increasing menu prices or compromising the customer experience.

As uncertainty over energy prices continues, staying informed and planning ahead is more important than trying to time the market. Iain Bailey, Director at Newgen Utility Solutions, explains:

“The market had been expecting only a short-lived disruption, with supply recovering by mid-2026, but that now looks increasingly unlikely. Gas supply can't be replaced quickly, so upward pressure on prices is building and electricity costs will follow.

Prices are still below the previous crisis peaks, but the direction of travel is clear, and it's worth being prepared for a tighter market over the coming months rather than assuming a return to recent lows.

The businesses best placed to respond are the ones that already know their usage and key contract dates, are clear on what's driving their decision — security of supply versus lowest price — and have started reviewing their options well in advance.”

For more advice on energy management, or to discuss how current market conditions are affecting your business, book a call with our team.

BBC (2026). Breaking Point for Hospitality

BBC (2026). Hospitality Bosses Cannot Afford New Staff

Brakes (2026). Crop Reports: May

Food and Drink Federation (2026). FDF Food Inflation Statement

NielsenIQ (2026). Mixed Weather Brings Soft Start to June

Office for National Statistics (2026). Consumer Price Inflation: May

Office for National Statistics (2026). Producer Price Inflation: May

Oliver Kay (2026). Summer Crop Report

The Guardian (2026). Pubs Serve 5.5m Extra Pints During World Cup